基于XGBoots预测A股大盘《上证指数》(代码+数据+一键可运行)

在股票预测中,AI充当着数据分析和模式识别的角色。虽然无法确保百分之百准确的结果,但它为增加预测的洞察力和理解提供了全新的途径。对AI炒股感兴趣的小伙伴可加WX:caihaihua057200(备注:学校/公司+名字+方向)在这期内容中,我们回到AI预测股票,转而探索人工智能技术如何应用于另一个有趣的领域:预测A股大盘。另外我还有些AI的应用可以一起研究(我一直开源代码)6、结果(预测下周上证:图

·

对AI炒股感兴趣的小伙伴可加WX:caihaihua057200(备注:学校/公司+名字+方向)

或者关注微信公众号《三个篱笆三个帮》我会在里面公开量化股池

另外我还有些AI的应用可以一起研究(我一直开源代码)

1、引言

在这期内容中,我们回到AI预测股票,转而探索人工智能技术如何应用于另一个有趣的领域:预测A股大盘。

2、AI与股票的关系

在股票预测中,AI充当着数据分析和模式识别的角色。虽然无法确保百分之百准确的结果,但它为增加预测的洞察力和理解提供了全新的途径。

3、数据收集与处理(akshare爬实时上证指数)

import akshare as ak

import numpy as np

import pandas as pd

from pandas.tseries.offsets import CustomBusinessDay

from datetime import datetime

import xgboost as xgb

df = ak.stock_zh_index_daily_em(symbol='sh000001') 数据预处理:时间特征转换及时间特征结合K线特征

today = datetime.today()

date_str = today.strftime("%Y%m%d")

base = int(datetime.strptime(date_str, "%Y%m%d").timestamp())

change1 = lambda x: (int(datetime.strptime(x, "%Y%m%d").timestamp()) - base) / 86400

change2 = lambda x: (datetime.strptime(str(x), "%Y%m%d")).day

change3 = lambda x: datetime.strptime(str(x), "%Y%m%d").weekday()

df['date'] = df['date'].str.replace('-', '')

X = df['date'].apply(lambda x: change1(x)).values.reshape(-1, 1)

X_month_day = df['date'].apply(lambda x: change2(x)).values.reshape(-1, 1)

X_week_day = df['date'].apply(lambda x: change3(x)).values.reshape(-1, 1)

XX = np.concatenate((X, X_week_day, X_month_day), axis=1)[29:]

FT = np.array(df.drop(columns=['date']))

min_vals = np.min(FT, axis=0)

max_vals = np.max(FT, axis=0)

FT = (FT - min_vals) / (max_vals - min_vals)

window_size = 30

num_rows, num_columns = FT.shape

new_num_rows = num_rows - window_size + 1

result1 = np.empty((new_num_rows, num_columns))

for i in range(new_num_rows):

window = FT[i: i + window_size]

window_mean = np.mean(window, axis=0)

result1[i] = window_mean

result2 = np.empty((new_num_rows, num_columns))

for i in range(new_num_rows):

window = FT[i: i + window_size]

window_mean = np.max(window, axis=0)

result2[i] = window_mean

result3 = np.empty((new_num_rows, num_columns))

for i in range(new_num_rows):

window = FT[i: i + window_size]

window_mean = np.min(window, axis=0)

result3[i] = window_mean

result4 = np.empty((new_num_rows, num_columns))

for i in range(new_num_rows):

window = FT[i: i + window_size]

window_mean = np.std(window, axis=0)

result4[i] = window_mean

result_list = [result1, result2, result3, result4]

result = np.hstack(result_list)

XX = np.concatenate((XX, result), axis=1)4、预测模型(XGboots)

y1 = df['open'][29:]

y2 = df['close'][29:]

y3 = df['high'][29:]

y4 = df['low'][29:]

models1 = xgb.XGBRegressor()

models2 = xgb.XGBRegressor()

models3 = xgb.XGBRegressor()

models4 = xgb.XGBRegressor()

models1.fit(XX, y1)

models2.fit(XX, y2)

models3.fit(XX, y3)

models4.fit(XX, y4)5、应用及画图

start_date = pd.to_datetime(today)

bday_cn = CustomBusinessDay(weekmask='Mon Tue Wed Thu Fri')

future_dates = pd.date_range(start=start_date, periods=6, freq=bday_cn)

future_dates_str = [date.strftime('%Y-%m-%d') for date in future_dates][1:]

future_dates_str = pd.Series(future_dates_str).str.replace('-', '')

X_x = future_dates_str.apply(lambda x: change1(x)).values.reshape(-1, 1)

X_month_day_x = future_dates_str.apply(lambda x: change2(x)).values.reshape(-1, 1)

X_week_day_x = future_dates_str.apply(lambda x: change3(x)).values.reshape(-1, 1)

XXX = np.concatenate((X_x, X_week_day_x, X_month_day_x), axis=1)

last_column = result[-1:, ]

repeated_last_column = np.tile(last_column, (5, 1))

result = repeated_last_column

XXX = np.concatenate((XXX, result), axis=1)

pred1 = models1.predict(XXX)

pred2 = models2.predict(XXX)

pred3 = models3.predict(XXX)

pred4 = models4.predict(XXX)

y1 = np.array(df['open'][-30:])

y2 = np.array(df['close'][-30:])

y3 = np.array(df['high'][-30:])

y4 = np.array(df['low'][-30:])

YD = np.array(df['date'][-30:])

data = {

'open': np.concatenate([y1, pred1]),

'close': np.concatenate([y2, pred2]),

'high': np.concatenate([y3, pred3]),

'low': np.concatenate([y4, pred4]),

'date':np.concatenate([YD,np.array(future_dates_str)])

}

df = pd.DataFrame(data)

import mplfinance as mpf

# df['date'] = pd.date_range(start=RQ, periods=len(df))

df['date'] = pd.to_datetime(df['date'])

df.set_index('date', inplace=True)

# mpf.plot(df, type='candle', title='Stock K-Line')

my_color = mpf.make_marketcolors(up='red', # 上涨时为红色

down='green', # 下跌时为绿色

# edge='i', # 隐藏k线边缘

# volume='in', # 成交量用同样的颜色

inherit=True)

my_style = mpf.make_mpf_style(

# gridaxis='both', # 设置网格

# gridstyle='-.',

# y_on_right=True,

marketcolors=my_color)

mpf.plot(df, type='candle',

style=my_style,

# datetime_format='%Y年%m月%d日',

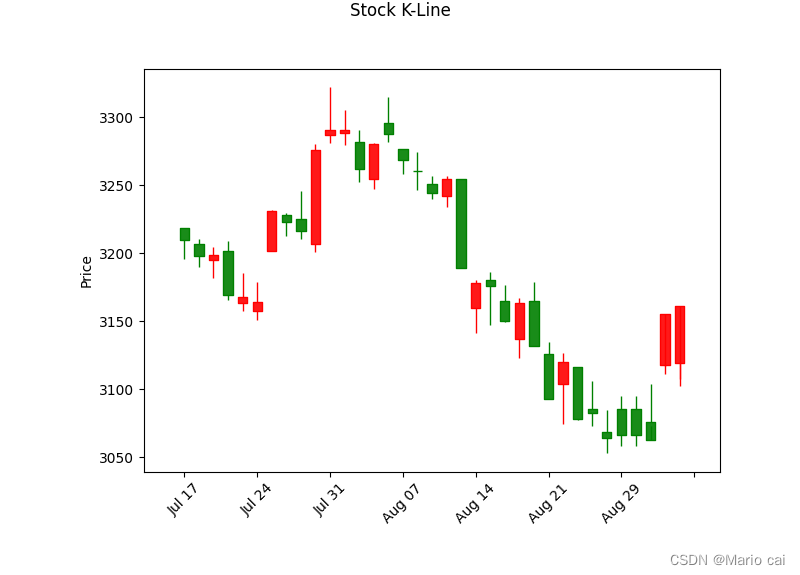

title='Stock K-Line')6、结果(预测下周上证:图中后五天是预测结果)

总结图中所示:

1、周一到周三略微上涨一点点。

2、下周四五高开高走(令人惊讶)。

如果提前布局的话应该是选择在周四找最低点买入。

全代码,一件运行:

import akshare as ak

import numpy as np

import pandas as pd

from pandas.tseries.offsets import CustomBusinessDay

from datetime import datetime

import xgboost as xgb

df = ak.stock_zh_index_daily_em(symbol='sh000001')

today = datetime.today()

date_str = today.strftime("%Y%m%d")

base = int(datetime.strptime(date_str, "%Y%m%d").timestamp())

change1 = lambda x: (int(datetime.strptime(x, "%Y%m%d").timestamp()) - base) / 86400

change2 = lambda x: (datetime.strptime(str(x), "%Y%m%d")).day

change3 = lambda x: datetime.strptime(str(x), "%Y%m%d").weekday()

df['date'] = df['date'].str.replace('-', '')

X = df['date'].apply(lambda x: change1(x)).values.reshape(-1, 1)

X_month_day = df['date'].apply(lambda x: change2(x)).values.reshape(-1, 1)

X_week_day = df['date'].apply(lambda x: change3(x)).values.reshape(-1, 1)

XX = np.concatenate((X, X_week_day, X_month_day), axis=1)[29:]

FT = np.array(df.drop(columns=['date']))

min_vals = np.min(FT, axis=0)

max_vals = np.max(FT, axis=0)

FT = (FT - min_vals) / (max_vals - min_vals)

window_size = 30

num_rows, num_columns = FT.shape

new_num_rows = num_rows - window_size + 1

result1 = np.empty((new_num_rows, num_columns))

for i in range(new_num_rows):

window = FT[i: i + window_size]

window_mean = np.mean(window, axis=0)

result1[i] = window_mean

result2 = np.empty((new_num_rows, num_columns))

for i in range(new_num_rows):

window = FT[i: i + window_size]

window_mean = np.max(window, axis=0)

result2[i] = window_mean

result3 = np.empty((new_num_rows, num_columns))

for i in range(new_num_rows):

window = FT[i: i + window_size]

window_mean = np.min(window, axis=0)

result3[i] = window_mean

result4 = np.empty((new_num_rows, num_columns))

for i in range(new_num_rows):

window = FT[i: i + window_size]

window_mean = np.std(window, axis=0)

result4[i] = window_mean

result_list = [result1, result2, result3, result4]

result = np.hstack(result_list)

XX = np.concatenate((XX, result), axis=1)

y1 = df['open'][29:]

y2 = df['close'][29:]

y3 = df['high'][29:]

y4 = df['low'][29:]

models1 = xgb.XGBRegressor()

models2 = xgb.XGBRegressor()

models3 = xgb.XGBRegressor()

models4 = xgb.XGBRegressor()

models1.fit(XX, y1)

models2.fit(XX, y2)

models3.fit(XX, y3)

models4.fit(XX, y4)

start_date = pd.to_datetime(today)

bday_cn = CustomBusinessDay(weekmask='Mon Tue Wed Thu Fri')

future_dates = pd.date_range(start=start_date, periods=6, freq=bday_cn)

future_dates_str = [date.strftime('%Y-%m-%d') for date in future_dates][1:]

future_dates_str = pd.Series(future_dates_str).str.replace('-', '')

X_x = future_dates_str.apply(lambda x: change1(x)).values.reshape(-1, 1)

X_month_day_x = future_dates_str.apply(lambda x: change2(x)).values.reshape(-1, 1)

X_week_day_x = future_dates_str.apply(lambda x: change3(x)).values.reshape(-1, 1)

XXX = np.concatenate((X_x, X_week_day_x, X_month_day_x), axis=1)

last_column = result[-1:, ]

repeated_last_column = np.tile(last_column, (5, 1))

result = repeated_last_column

XXX = np.concatenate((XXX, result), axis=1)

pred1 = models1.predict(XXX)

pred2 = models2.predict(XXX)

pred3 = models3.predict(XXX)

pred4 = models4.predict(XXX)

y1 = np.array(df['open'][-30:])

y2 = np.array(df['close'][-30:])

y3 = np.array(df['high'][-30:])

y4 = np.array(df['low'][-30:])

YD = np.array(df['date'][-30:])

data = {

'open': np.concatenate([y1, pred1]),

'close': np.concatenate([y2, pred2]),

'high': np.concatenate([y3, pred3]),

'low': np.concatenate([y4, pred4]),

'date':np.concatenate([YD,np.array(future_dates_str)])

}

df = pd.DataFrame(data)

import mplfinance as mpf

# df['date'] = pd.date_range(start=RQ, periods=len(df))

df['date'] = pd.to_datetime(df['date'])

df.set_index('date', inplace=True)

# mpf.plot(df, type='candle', title='Stock K-Line')

my_color = mpf.make_marketcolors(up='red', # 上涨时为红色

down='green', # 下跌时为绿色

# edge='i', # 隐藏k线边缘

# volume='in', # 成交量用同样的颜色

inherit=True)

my_style = mpf.make_mpf_style(

# gridaxis='both', # 设置网格

# gridstyle='-.',

# y_on_right=True,

marketcolors=my_color)

mpf.plot(df, type='candle',

style=my_style,

# datetime_format='%Y年%m月%d日',

title='Stock K-Line')

CSDN联合极客时间,共同打造面向开发者的精品内容学习社区,助力成长!

更多推荐

2

2 0

0- 0

已为社区贡献3条内容

已为社区贡献3条内容

所有评论(0)